Featured Vendor

This section briefly explains IDC’s key observations resulting in a vendor’s position in the IDC MarketScape. While every vendor is evaluated against each of the criteria outlined in the Appendix, the description here provides a summary of each vendor’s strengths and challenges.

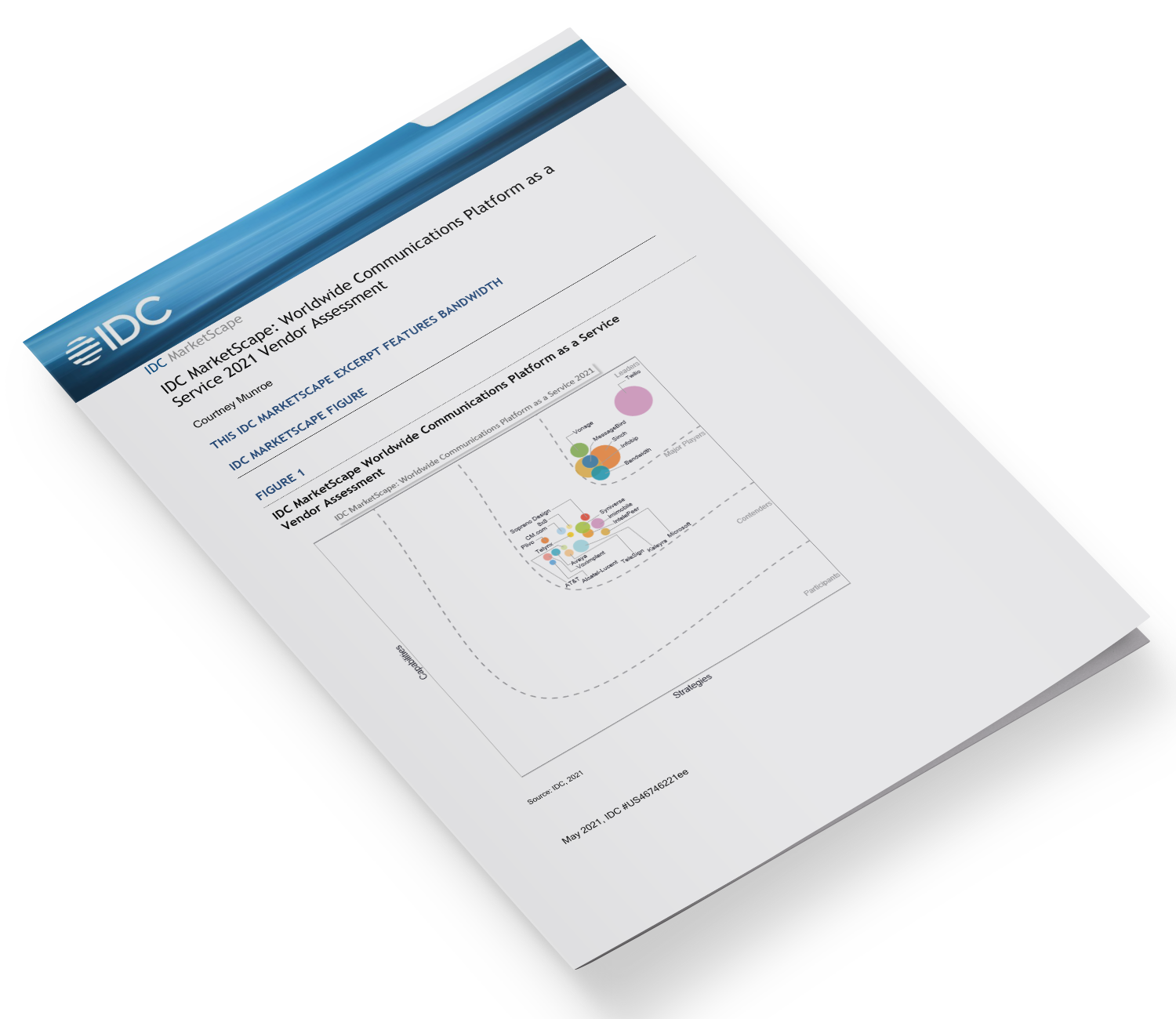

Bandwidth

Bandwidth is positioned in the Leaders category in the 2021 IDC MarketScape for the worldwide CPaaS market.

Bandwidth has a global IP network with a cloud platform layer that delivers a portfolio of voice, messaging, phone numbers, and 911 capabilities. Bandwidth has established a reputation as a reliable scalable platform that offers a robust voice platform for a diverse array of cloud providers. The company emerged from 2020, second only to Twilio in growing its YoY organic revenue by 50%. The 2020 acquisition of Voxbone extends its capability to a global scale with the addition of another 60 countries. The company is now a national licensed operator in several markets, including most European Union (EU) countries.

Strengths

Bandwidth’s key differentiator is its global IP backbone. As a tier 1 provider with its own network, Bandwidth has significant flexibility to scale and can guarantee carrier- and enterprise-grade quality as well as optimal and cost-effective routing. The merger with Voxbone provides additional scale, talent, and opportunities to gain share in new markets. In addition to its traditional portfolio of voice, 911, and phone numbers, Bandwidth offers an expanded catalog of IP services and APIs to facilitate enterprise telephony and customer engagement strategies. It offers integrations for BYOC with Microsoft Teams, Genesys, and other CCaaS platforms, and it supports several popular UCaaS companies. Looking to the future the company has initiated a wave of enhancement and new solutions. It has a video API in beta and will also introduce an authentication API and branded SMS and voice calling. Bandwidth will also introduce new billing and real-time analytical capabilities during 2021.

Challenges

Bandwidth is undergoing immense transformation and growth. It is simultaneously integrating a new entity into the company and releasing several new solutions and enhancements to its portfolio during 2021. If Bandwidth can manage a smooth integration of Voxbone and its planned enhancements, it will be poised for several years of strong growth.

Consider Bandwidth When

Your company is seeking a reliable carrier-grade voice platform with integrations into popular CCaaS and UC platform and deep trove and expertise in phone numbers. Bandwidth’s global footprint and expanding portfolio also presents a CPaaS partner that offers immense opportunities to scale and expand channels as needed.